Welcome to the Beginner’s Guide to Applying for Multiple Credit Cards! This is a step-by-step guide to show you how to get ready and apply for credit cards to earn airline miles & credit card points. The series will consist of 4 posts that cover these basic topics:

Part 1: Check and review your credit score

Part 2: Evaluate current credit cards and choose the best new cards

Part 3: Results and what do if your application goes pending

Part 4: Stay organized and monitor your credit

As I get ready to launch another round of credit card applications I figured it would be a perfect time to write a post detailing the process that I use when I apply for multiple credit cards. The guide will be written from my perspective and how I go about each process. This guide is geared towards person new to applying to credit cards to earn points, so if you are more experienced feel free to skim over it as a refresher.

The last round of credit card applications I submitted was back in April, when I applied for 6 cards and earned 370,000 miles and points. Since then I have been fairly busy with traveling and school so in the mean time I’ve been waiting for some hard inquiries to drop off from my credit history before I applied for any new offers. There are several offers available that I want to apply for making it good time to do so. This round of card applications will not be as big as the last one, but I still hope to get approved for 2-3 new cards to earn some points to refill my accounts after my month long trip to Turkey and Croatia this summer.

There are several steps that I always include before I start a round of card applications: review my credit score, evaluate the current cards I have and decide which ones to keep or to cancel, and choose which top offers will benefit me the most during this application round. It is essential that everything is in order before clicking the submit button on multiple applications. After all, you want to get approved for as many cards as possible and ultimately earn thousands of miles and points to use for future travel.

Building and maintaining a healthy credit profile is an essential part of successfully earning credit card welcome bonuses. The following review of credit scores aims to demystify the complexities of a credit score and provide simple strategies to monitor it, evaluate it, and maintain a high score.

What is a FICO Score?

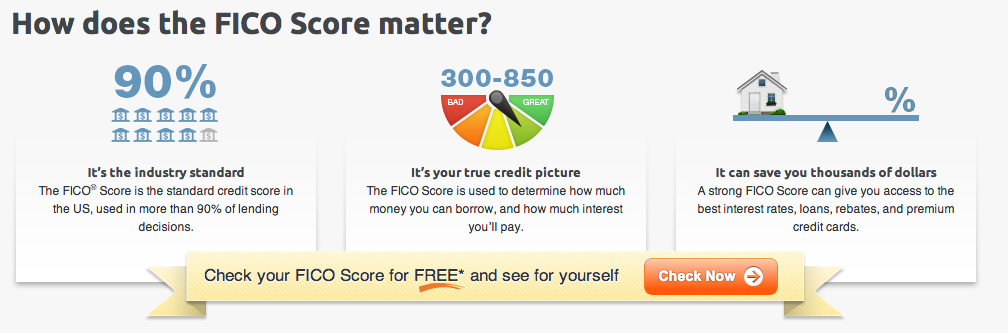

The Fair Isaac Company or FICO, collects all of your credit information from loans, credit card history, late payments, etc. and summarizes your credit history to sell back to entities that request a credit check. The industry standard for evaluating your credit worthiness is the FICO score, so banks always take a look at your score when evaluating whether or not to approve you for a new credit card.

VantageScore is another credit-scoring company, and you will see this listed when you monitor your credit score on Credit Sesame, Quizzle, or Credit Karma. The VantageScore is less widely recognized than the FICO score, so FICO scores are the basis of what you should judge your credit on.

FICO scores range between 300-850, and the Fair Isaac Company uses multiple indicators to calculator each persons individual score within this range. Banks have chosen to use the FICO score as the standard in order to compare apples-to-apples when comparing credit. This way a company can look at your FICO score and place your score in this range to judge whether or not to approve you for a credit card or loan. Having a high FICO score is the best indicator of whether your card applications will be approved or denied.

Credit Karma uses FAKO score that seems to be fairly accurate when compared to your FICO score. The range of scores seen on Credit Karma are the same, 300-850. They also offer a grade rating, which runs from A to F.

Based on that range, it appears that the grades correspond roughly to:

750 – 850: A or Excellent

700 – 749: B or Good

630 – 699: C or Average

580 – 629: D or Below Average

300 – 529: F or Bad

A “Good” credit score is generally over 700 and will allow you to get approved for most premium credit cards. Credit card companies generally don’t differentiate much among scores between 720-850 and I have heard that banks treat any score over 720 essentially the same.

However, there are many variables that are taken into account and your total credit history is reviewed when credit card companies evaluate you for approval. The credit score industry remains very secretive, and the minimum credit score that credit card issuers accept is kept secret. Finding out any hard facts about credit scores remains very elusive and the only way to find out if you will be approved for a card is after you hit the submit button on an application.

The entire credit scoring system and what is needed to be approved for credit cards is generally kept very vague and there are no definite answers for most questions that people have. There are however, great resources such as the numerous miles and points forums and blogs that provide personal feedback from trial and error. These resources are a great way to begin to understand what is needed to qualify for credit card offers. You can also do more research on creditboards.com.

Presumably, with the information collected from submitted applications, Credit Karma publishes the average and minimum credit score approved for specific cards. These can be great indicators to decide which card to apply for, but they still do not guarantee that you will be approved for the card.

How Is Your FICO Score Calculated?

The easiest way to understand a FICO score is to break it down by the five main factors that influence the score.

35% of your credit based on your payment history. This is the largest factor that determines your credit score, and is simply based on whether or not you pay off your bills (credit card, mortgages, etc) in full. For this reason it is vital to pay off your bills and credit card in full every month to maintain a strong credit score. If you are not diligent about paying off your credit card every month in full, then the points and miles game is not for you.

30% is based on the amount you owe. Included in this are the types of accounts you owe them on, credit utilization, and other debt related items. This means that the record of the balances you carry has almost as much impact to your credit score as your payment history. Your credit utilization is used by determining the proportion of your credit lines that you use. Generally, the higher the amount you owe in relation to the total amount of credit, lower your credit score.

15% of your credit score is determined by the length of your credit history. It is based on how long you’ve had certain types of accounts and the time since your last activity. The longer you have maintained active accounts, the higher credit score. This is why it is a great idea to start building your credit history as early as possible, and maintaining the oldest account you have open to help the average credit length. I suggest to always keep a credit card with a zero annual fee open to maintain a long credit life of your oldest card.

10% of your credit score is calculated by any new lines of credit. This can be in the form of a credit card, mortgage, or a loan. Also included in this are new credit inquiries–this is why after applying for a mortgage or recently going through a lot of credit card applications, your score may drop several points. Since credit inquiries diminish over time the impacts generally disappear from your credit report after 3 months.

10% of your credit score is based on all the types of credit you use. Included in this are all the different types of credit accounts you have, including credit cards, loans, mortgages, and any other lines of credit.

All five of these factors play a role in determining your FICO score and each holds a different weight. It’s clear as to which factors have the largest influence and others that are less important. With that being said, they all influence your credit score and the better your standing is in each section will account for a higher overall credit score. You certainly don’t have to have a perfect history in all of these areas to have a score above 700. It is good to know what factors influence your score when your are building your credit score.

Best Ways To Get Your Credit Score

Before applying for credit cards it is vital to know your current credit score. You want to know that your score is high enough that you will likely get approved for the cards you apply for. It is also good practice to keep track of your score before and after credit card applications.

There are several easy ways to monitor your credit score:

annualcreditreport.com – If you live in the US, every year you are eligible for one free credit report from each of the three major credit reporting bureaus –TransUnion, Experian and Equifax. You will only get a credit report that shows your history and activity, for an accurate score you must pay $19.95 through myfico.com (remember that FICO is a profit driven company).

Credit Sesame, Quizzle, and Credit Karma – All of these websites provide a free estimated credit score known as a FAKO score. Credit Sesame uses an Experian proxy and Credit Karma uses a TransUnion proxy–both are fairly accurate but you may see slight variations between the two scores.

Other useful tools on these sites show recent credit inquiries, risk analysis, and account activity. Because this is not a FICO score, it is not the EXACT score credit card companies will see when you apply for a card, but it offers a good estimate for you to use before applying. These websites make it simple and easy to track your credit score and activity before, during, and after applying for credit cards and since they are free, you can check your score as much as your want. Your credit will not be affected by checking your score on either of these site, so feel free to check it as often as you want.

Quick Recap

When the goal is to earn miles and points checking your credit score is an essential first step when applying for multiple credit card applications. There are no definite answers when it comes to determining how your score is exactly calculated or if you wil be approved for a card. The best strategy is to use the tools mentioned in this post, and understand the factors affecting your credit score. Using these you can decide what you can do to improve your score if your score is being affected by one of these areas. Remember that the most integral part to building and maintaining a high credit score is to pay off your balance in full every month. A high score you will enable you to take advantage of free travel from earning thousands of points from credit card offers.

* If you found this post useful, why don’t sign-up to receive free blog posts via email (max of 1 email per day!) or like us on Facebook…and never miss an update!