Don’t forget to follow me on Twitter or Facebook!

This is the second post of a four part series that will walk you through the steps to multiple credit card applications to earn miles and points. This post will focus on how to conduct a personal credit card inventory and how to evaluate which cards to keep and those to cancel. The first post covered the basics on preparing for the application process and double checking your credit health to ensure that everything is up to par before applying for credit cards. The 3rd post will be a summary of my recent applications, including the results, and dealing with the reconsideration lines. I will have a final and 4th post analyzing the impacts of my credit score and how credit card applications affects it.

Half the process of applying for multiple credit cards is determining which credit cards are the best options for you.

At any given time there are really good offers that you want to get your hands on, but you have to narrow down the list of cards you want to go for to improve your chances of being approved for the ones highest on your list.

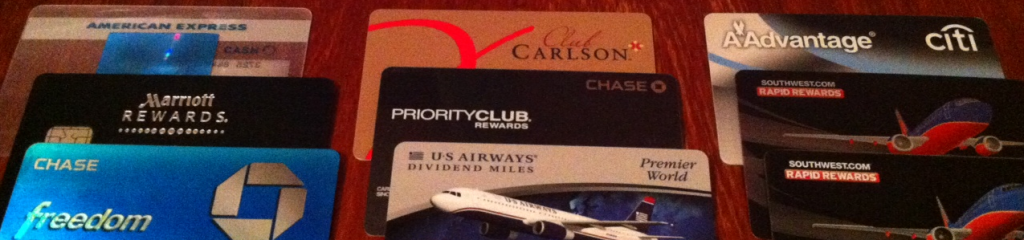

To start this process, I like to take a glance at the cards I currently have which helps me determine what cards are not worth keeping, as well as what cards to apply for to earn points or other benefits.

Take a look at what’s in your wallet

I like to go through my cards and evaluate each card with these questions:

Does the card have an annual fee and do I want to pay it for another year? Are the benefits of each card worth more than the annual fee? I normally don’t like to keep too many cards a second year because the annual fees will hit. There are some cards that are clearly worth the annual fee because of the benefits and annual bonus, such as free hotel nights or points. The Club Carlson Visa has a 40k anniversary bonus, which is worth close to 2 free nights at a top tier property–well worth the $75 annual fee.

Can I replace a card with a new one that give me close to the same benefits but will net me a new welcome bonus? Some cards either change their name or are offered in various versions so you can potentially apply for a new version of the card and get similar benefits as well as a new welcome bonus. The Southwest Rapid Rewards cards with the 50,000 points bonus are offered in four different versions, and you can earn the bonus for all four cards because Chase considers them different products.

How old is the credit card account? I always keep my two oldest cards to help extend my averaged credit length, which helps keep a high credit score. None of my oldest cards have an annual fee so I plan on keeping them indefinitely for this purpose as they do count for 15% of my credit score.

Do the benefits of the card fulfill my needs/goals? Based on your own values, principles and goals the types of perks and benefits you aim for will vary. For me, travel benefits are my number one goal, but for others it might be cashback earnings and points for statement credits or other purchases. On this round of credit card applications I want to focus on hotel points and free nights. I feel pretty good about my airline mile balances, and want to bring up my hotel rewards to match. A majority of the cards I plan on applying for are hotel credit cards, and I may cancel out a airline card or two.

After running a quick cost/benefit analysis on each of my credit cards and taking inventory on all the cards I have, I decided to cancel only one card–my Capital One Venture card. I have had this card for a couple years and really only use it for a couple purchases a year. I decided to cancel it and hope that someday in the future there will be another rare bonus offer for the card. I like to cancel cards that I am not using so I can earn another bonus offer in 12-20 months on the same card (Chase is the only bank that will not allow this).

Choosing which cards to apply for

Current top offers

The next step is to round up all potential mega welcome bonuss that are currently offered. At first make a list of all the potential offers, then you can narrow them down by evaluating each of them based on the value of the offer to you, the minimum spend, the annual fee, and your general travel goals.

Total minimum spends

Another thing to consider when choosing which cards to apply for is the minimum spend required for the welcome bonus. The key is to not bite off more than you can chew. Add up all the minimum spends of the new cards you are looking at getting and ask yourself if you can realistically reach these within three months. Along with everyday spending there are many ways to help you reach these such as Vanilla Reloads and Amazon payments.

I plan on meeting about $6,000-9,000 in minimum spends by a combination of Amazon Payments, Vanilla Reloads and everyday/business expenses all put on my new cards. I always put every possible purchase onto my cards–from household bills, dining, buying gas and making advanced payments sometimes if possible.

Putting a value on different miles and points

My use for miles and points will likely differ from yours–I tend to maximize the number trips and hotel stays by flying economy (with the occasional business class award flight) and staying in lower tiered properties. My favorite redemption for international travel is using United’s Mileage Plus miles (Star Alliance) to take advantaged of the open jaws and international stopovers. For trips to South and Central America I like using American Airlines AAdvantage miles because LAN is part of One World and taxes and fees tend to be very low.

When placing a value on miles and points you should determine your needs–do you want to travel international? Only fly in business class? Are most of your flights domestic? Do you like staying in the nicest hotels or are you willing to maximize your nights by staying in lower tier hotels? Use some of these questions to help you determine which bonus will fit your needs the most and the one that you are more likely to enjoy and use on an amazing trip.

In my opinion the most United’s miles and Club Carlson’s points are the most valuable and useful airline miles and hotel points right now.

First year annual fee waived?

I always try to avoid paying an annual fee when applying for new cards, but if the offer is good enough I will happily pay the first year’s fee for a flight or hotel stay valued at $500+. The Club Carlson Visa has a $75 fee for the first year and offers 85,000 points that can be redeemed for four free nights (worth $1,200+) at a top tier Radisson Blu in Europe.

Use credit lines to your advantage–transfer credit to get approved

If you already have multiple credit cards from one bank you can ask to transfer some of the credit from an existing card to allow the new one to be opened. This works particularly well with Chase when calling into the reconsideration line. I always mention that I wouldn’t mind if they transfered some existing credit from another card to approve the new card.

Focus on aggregating points/programs

Try to find several cards that will allow you to earn miles or points for the same airline or hotel loyalty program. I chose to apply for the Barclays US Airways Mastercard because once the AA merger goes there those miles will be combined with my AAdvantage Miles.

You can also apply for different versions of the card, such as the Southwest Rapid Rewards cards offered by Chase. There are four versions that you can earn bonuses for–both a personal and business card for the plus and premier version. Each of these cards are considered a different product by Chase, allowing you to earn a total of 200k Southwest points.

Stay tuned to see which cards I chose and why–and whether I got approved or not!

* If you found this post useful, why don’t sign-up to receive free blog posts via email (max of 1 email per day!) or in a RSS reader …be sure you’ll never miss another update!

Right now I have five chase credit cards, two of which are business cards. Would it be a good idea to cancel my southwest and united business accounts so that I can apply for more chase cards??

@ Erin – Chase generally won’t approve you for another card if you already have 4-5 cards with them. I currently have four personal and one business, and had to call into the reconsideration line to ask if they could shift some credit from an existing card in order get approved for the new card during my most recent round of credit card applications. Before applying, it might be a good idea to cancel one of your cards that you dont want anymore, or you can always call in after and ask to transfer some of your credit line from an existing card. Good luck!